Coordinate Fraud Prevention and Mobile Security Teams

Coordinated fraud prevention for mobile security teams is defined as the deliberate alignment of fraud detection, mobile runtime protection, and anti-money laundering (AML) functions into a unified operational model that shares risk signals in real time. Without this alignment, organizations face fragmented defenses against threats like smishing, executive impersonation, and credential harvesting that exploit gaps between siloed teams. Platforms like Appdome and Unit21 have demonstrated that coordinated mobile app security enables real-time risk signal sharing among backend fraud engines, increasing both detection accuracy and operational control. This article gives fraud prevention teams a concrete framework for building that coordination, from organizational structure through technology integration to continuous threat adaptation.

How should you structure teams to coordinate fraud prevention and mobile security?

The hybrid centralized-distributed model is the most effective organizational structure for fraud prevention and mobile security coordination in 2026. Research confirms that the hybrid model combining centralized expertise with distributed business unit teams mitigates risk while preserving specialization. A central fraud operations center sets policy, owns tooling, and maintains shared KPIs. Distributed teams embedded in product lines or geographic units apply those policies to their specific risk profiles.

Roles within this model need clear ownership to avoid duplication and blind spots. A well-structured fraud prevention team typically includes:

- Fraud Operations Lead: Owns detection rules, escalation protocols, and cross-functional KPIs

- Mobile Security Engineer: Manages runtime application self-protection (RASP) integration, CI/CD pipeline security, and device telemetry

- AML Analyst: Monitors transaction patterns for regulatory reporting and feeds risk context back to fraud teams

- Threat Intelligence Analyst: Tracks emerging attack campaigns, including smishing and SIM swapping, and updates detection logic accordingly

- Incident Responder: Executes containment actions such as session blocking and step-up authentication triggers

Senior fraud prevention roles now require 5 to 8 years of experience including SOP development and cross-functional leadership. This reflects a broader shift: the field now prioritizes behavioral analytics expertise and threat mitigation leadership over narrow tool proficiency.

The most common failure in this structure is misaligned KPIs. When fraud teams measure false positive rates and AML teams measure suspicious activity report (SAR) volume, neither team has an incentive to share data. Shared metrics, such as time-to-detect and cross-channel fraud loss, create the organizational gravity that pulls teams together.

Pro Tip: Set a monthly cross-functional review where fraud, mobile security, and AML teams present their top three active threat patterns. This single ritual surfaces more coordination gaps than any governance document.

How can device intelligence and embedded app protections prevent mobile fraud?

Device intelligence is the practice of analyzing device type, behavior, geolocation, and prior fraud associations to produce a risk score before a transaction is approved. According to Unit21, early device risk scoring reduces false positives and fraud losses by enabling risk decisions earlier in the session lifecycle. That early signal is the difference between stopping a smishing-driven account takeover at login and chasing it after funds move.

The table below compares traditional server-side detection with embedded runtime protection, two approaches that must work together rather than replace each other.

| Capability | Server-side detection | Embedded runtime protection (RASP) |

|---|---|---|

| Visibility scope | Network traffic and API calls | In-app behavior, memory, and environment |

| Bot detection | Limited against mobile bots | Detects emulators, hooking frameworks, and tampered environments |

| Latency | Post-request analysis | Real-time, in-session |

| Bypass risk | High for AI-driven mobile bots | Low when embedded at build time via CI/CD |

| Fraud signal output | Transaction-level | Session-level and device-level combined |

AI-driven mobile bots bypass traditional defenses like CAPTCHAs and server-side analysis, which means runtime visibility inside the app binary is no longer optional. Embedding RASP protections during the CI/CD build process prevents fraud at the source rather than reacting after the fact. Appdome’s approach integrates these protections without requiring developers to write security code manually, which removes a common bottleneck in security team coordination.

Device intelligence must also be integrated directly into fraud decision engines. Siloed raw device fingerprinting creates inefficiencies because fraud analysts cannot act on data they cannot interpret. Transparent device risk scoring, surfaced inside the fraud workflow, allows analysts to adjust risk thresholds dynamically without waiting for engineering support.

Pro Tip: When evaluating device intelligence vendors, require that risk scores be available as a real-time API field inside your fraud decision engine, not just as a separate dashboard. Analysts who must context-switch between tools will miss signals under pressure.

Why breaking silos between fraud and AML teams improves mobile fraud mitigation

Fraud and AML teams share a subject but operate on different timelines and regulatory mandates. Fraud focuses on stopping immediate financial harm. AML focuses on detecting patterns that indicate money laundering and generating regulatory reports. Sharing data and risk context between these functions reduces blind spots that sophisticated fraud actors deliberately exploit.

The practical overlap is significant. A smishing campaign that harvests credentials and initiates unauthorized transfers generates both a fraud event and a potential SAR trigger. When fraud and AML teams investigate separately, they often reconstruct the same attack chain twice, wasting resources and missing the full picture of a coordinated criminal operation.

Breaking down these silos produces measurable operational benefits:

- Unified case management: A single investigation record that both fraud and AML analysts can annotate prevents duplicate work and preserves audit trails

- Shared risk signals: Device risk scores, behavioral anomalies, and network flags generated by fraud detection feed directly into AML transaction monitoring rules

- Cross-functional escalation paths: When a fraud signal crosses a regulatory threshold, a defined handoff protocol moves the case to AML without data loss

- Combined platform efficiency: Combining fraud detection with AML reporting in a single platform increases audit readiness and organizational transparency

Failure to coordinate these teams produces disconnected investigations and overlooked criminal activity. Unit21’s research on AML and fraud overlap shows that organizations running separate systems for each function consistently miss multi-stage fraud schemes that cross the boundary between the two disciplines. The mobile attack surface amplifies this problem because smishing and messaging-based social engineering attacks initiate outside the corporate perimeter, where neither fraud nor AML teams have default visibility.

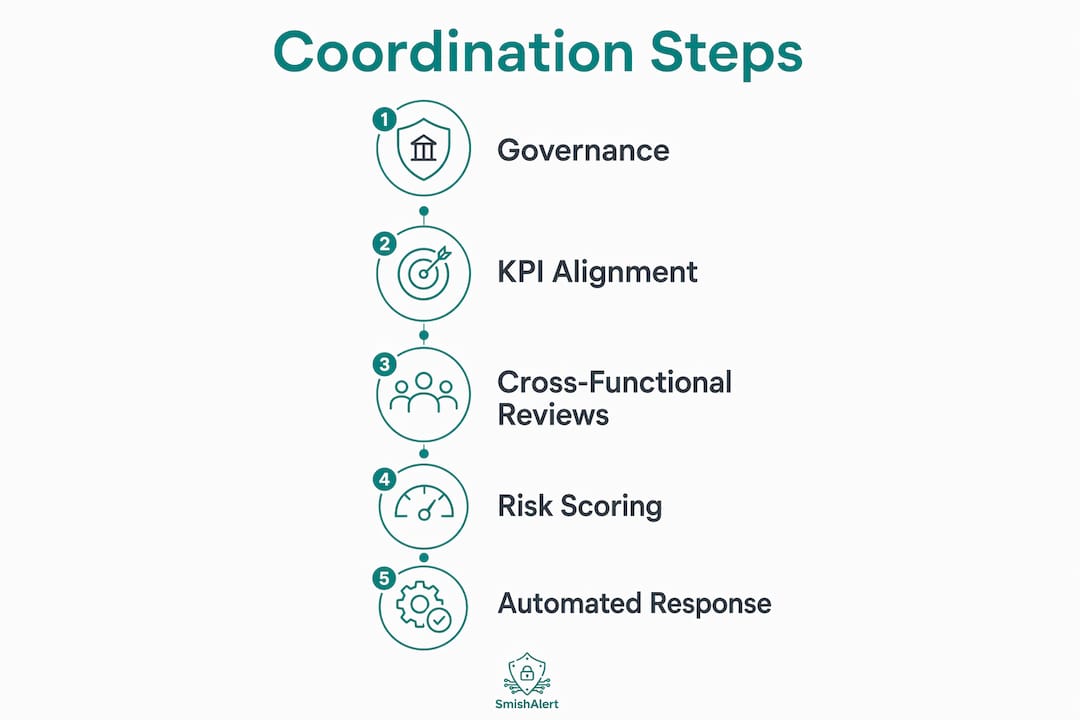

What practical steps build coordination among mobile fraud prevention teams?

Building durable coordination requires governance, technology integration, and a continuous improvement loop. The following steps give security leaders a structured path from fragmented operations to unified mobile fraud response.

-

Establish a cross-functional governance charter. Define which team owns each detection layer, who approves rule changes, and how escalations move between fraud, mobile security, and AML. Without written accountability, coordination collapses under incident pressure.

-

Integrate device intelligence into your fraud decision engine. Connect device risk scores from tools like Unit21 or similar platforms directly into your rule engine as a real-time input field. This allows fraud analysts to act on device signals without engineering intervention.

-

Embed RASP protections in the mobile app build pipeline. Work with mobile security engineers to add runtime protections during CI/CD. Platforms like Appdome automate this without requiring code changes, which removes the friction that typically delays security integration.

-

Implement automated response triggers. Automatically triggering step-up authentication or session blocking based on network risk signals prevents account takeover and smishing fraud more effectively than SMS OTP alone. Silent identity verification addresses SIM swapping exploits that OTP cannot stop.

-

Monitor messaging-based threats continuously. Smishing campaigns evolve faster than quarterly review cycles. Assign a threat intelligence analyst to track active SMS, iMessage, and WhatsApp attack campaigns and push rule updates to fraud detection systems within 24 hours of a new pattern emerging.

The table below maps each coordination step to its primary owner and the metric that confirms it is working.

| Coordination step | Primary owner | Success metric |

|---|---|---|

| Governance charter | Fraud Operations Lead | Escalation resolution time under 4 hours |

| Device intelligence integration | Mobile Security Engineer | False positive rate reduction of 15% or more |

| RASP embedding in CI/CD | Mobile Security Engineer | Zero unprotected app builds in production |

| Automated response triggers | Fraud Operations Lead | Account takeover rate month-over-month |

| Messaging threat monitoring | Threat Intelligence Analyst | Rule update latency under 24 hours |

Leading fraud platforms monitor over 1 billion devices and process 357,000 or more API calls daily to improve detection accuracy. That scale is only useful if your team has the governance and integration architecture to act on the signals it produces.

Key takeaways

Effective coordination of fraud prevention and mobile security teams requires unified governance, embedded runtime protections, shared device intelligence, and aligned fraud and AML workflows operating as a single defense system.

| Point | Details |

|---|---|

| Hybrid team structure | Combine centralized policy ownership with distributed business unit teams for scalable fraud defense. |

| Device intelligence integration | Surface device risk scores inside fraud decision engines so analysts can act without engineering delays. |

| Embedded runtime protection | Add RASP to mobile apps during CI/CD builds to detect bots, emulators, and tampered environments in real time. |

| Fraud and AML alignment | Share risk signals and case records between fraud and AML teams to close investigation gaps on complex schemes. |

| Automated response protocols | Trigger step-up authentication and session blocking automatically based on device and network risk signals. |

What I’ve learned about coordination that most frameworks miss

I’ve reviewed a lot of mobile security fraud strategy documentation over the years, and the gap between what organizations plan and what they actually execute comes down to one thing: tool integration is not the same as team coordination. Security leaders invest in platforms like Appdome, Unit21, and SIEM systems, connect the APIs, and declare the problem solved. Six months later, fraud analysts are still working from a separate dashboard, AML is still filing SARs without fraud context, and the mobile security engineer is the only person who understands what the RASP telemetry means.

The organizations that actually close this gap share one structural habit: they treat coordination as an operational discipline, not a technology outcome. That means weekly cross-team threat reviews, shared KPIs that create mutual accountability, and escalation protocols that are practiced before an incident, not written during one. It also means accepting that AI-powered fraud will outpace any static rule set, so the team’s ability to update detection logic faster than attackers iterate is the real competitive advantage.

The smishing threat specifically exposes how poorly most organizations coordinate their human layer defenses. Employees receive a fraudulent SMS, click a credential-harvesting link, and the attack chain completes before any backend system fires an alert. The fix is not purely technical. It requires fraud teams, mobile security, and HR to share threat intelligence about active campaigns targeting employees, which is a coordination problem, not a tool problem.

— Sophie

How SmishAlert supports coordinated mobile fraud prevention

SmishAlert gives fraud prevention teams the visibility layer that backend fraud engines cannot provide on their own. The platform captures, correlates, and reports on social engineering attacks delivered through SMS, iMessage, WhatsApp, and other messaging channels, including smishing campaigns targeting employees with executive impersonation, credential harvesting, and payroll fraud lures. Through user reporting, threat analysis, and campaign correlation, SmishAlert surfaces attack patterns before they result in compromise. Security teams can feed SmishAlert’s threat intelligence directly into their fraud detection workflows via API, closing the gap between the human attack surface and backend risk engines. Explore the SmishAlert platform to see how it integrates with your existing fraud prevention and mobile security operations.

FAQ

What does it mean to coordinate fraud prevention and mobile security teams?

Coordinating fraud prevention and mobile security teams means aligning detection rules, risk signal sharing, and response protocols across fraud operations, mobile security engineering, and AML functions into a single operational model. The goal is to eliminate the gaps that attackers exploit when these functions operate independently.

Why is device intelligence critical for mobile fraud prevention?

Device intelligence provides early risk scoring based on device type, behavior, geolocation, and fraud history, allowing fraud teams to make risk decisions before a transaction completes. Integrated directly into fraud decision engines, it reduces false positives and accelerates response without requiring engineering support for each rule change.

How does smishing fit into a coordinated mobile fraud response?

Smishing attacks initiate outside the corporate perimeter through SMS and messaging apps, which means they are invisible to traditional email security and many backend fraud systems. Coordinated mobile fraud response requires threat intelligence feeds that capture active smishing campaigns and push detection updates to fraud rules within hours of a new pattern emerging.

What is the difference between fraud prevention and AML, and why does coordination matter?

Fraud prevention focuses on stopping immediate financial harm to customers or the organization. AML focuses on detecting money laundering patterns and generating regulatory reports. Coordination matters because complex fraud schemes cross both domains, and disconnected investigations allow criminal activity to go undetected at the boundary between the two functions.

How should organizations trigger automated responses to mobile fraud signals?

Organizations should configure fraud decision engines to automatically trigger step-up authentication or session blocking when device intelligence or network risk signals exceed defined thresholds. Silent identity verification methods are more effective than SMS OTP alone because they address SIM swapping exploits that one-time passwords cannot prevent.