Mobile Messaging Security: Meet Regulatory Requirements

Regulated industries are under mounting pressure to meet regulatory requirements for mobile messaging security as smishing attacks grow more sophisticated and enforcement actions multiply. A single unauthorized text message can trigger TCPA fines between $500 and $1,500, and that math scales brutally across a campaign. Beyond financial penalties, regulators now expect near-real-time visibility into messaging communications, tamper-evident archiving, and documented consent workflows. This guide gives compliance officers and security professionals a structured path through the regulatory terrain, from understanding which frameworks apply to deploying controls that actually hold up under audit.

Table of Contents

Key takeaways

| Point | Details |

|---|---|

| TCPA fines compound fast | Each unauthorized text carries a $500 to $1,500 penalty, making mass messaging errors catastrophically expensive. |

| Device ownership is irrelevant | Message content determines record retention obligations, regardless of whether a personal or company device sent it. |

| Encryption alone is not enough | MLS and TLS protect the channel but do not stop AI-driven impersonation; identity verification is required. |

| Automated archiving is mandatory | Regulators expect tamper-evident logs capturing edits and deletions, not screenshots or manual exports. |

| Smishing is a compliance gap | Inbound phishing attacks targeting employees create both security and regulatory exposure that legacy tools miss entirely. |

Meeting regulatory requirements for mobile messaging security

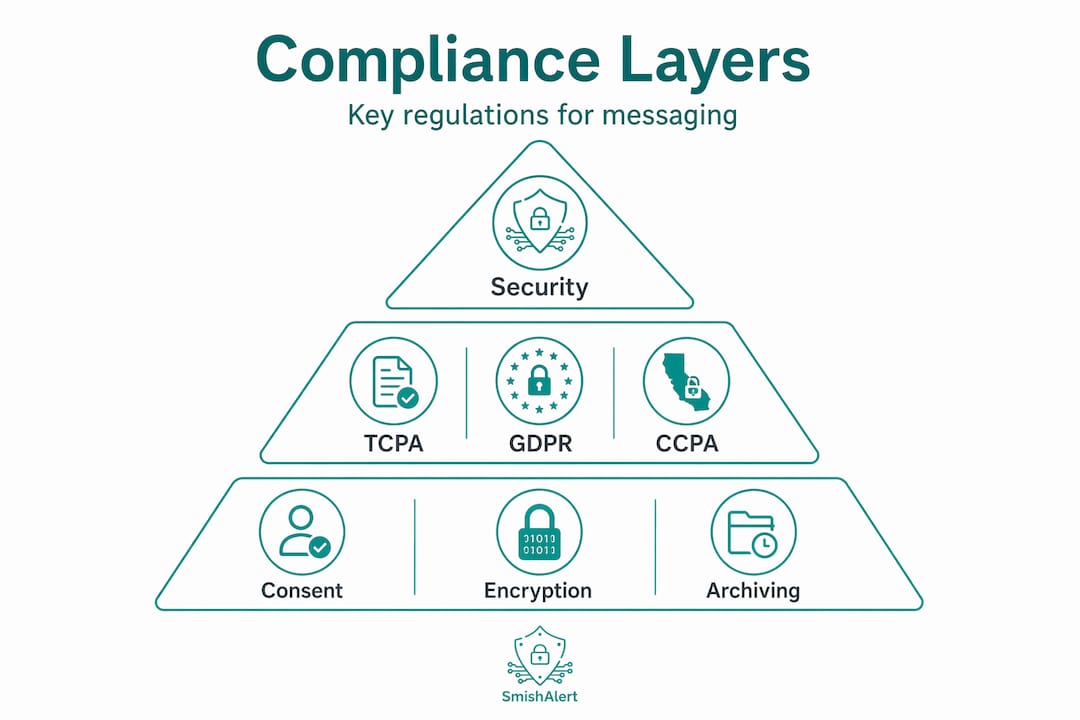

The regulatory framework governing mobile messaging in 2026 is not a single law. It is a layered stack of federal statutes, industry rules, and emerging technical standards that compliance teams must reconcile simultaneously.

The Telephone Consumer Protection Act (TCPA) governs consent and opt-out obligations for outbound messaging in the United States. The General Data Protection Regulation (GDPR) and the California Consumer Privacy Act (CCPA) impose data minimization, retention limits, and subject rights requirements on message content and metadata. Industry-specific rules add another layer: FINRA and SEC regulations require broker-dealers to archive all business communications, including those conducted over SMS and messaging apps, with metadata integrity preserved.

The table below maps the most common regulatory obligations to their technical requirements:

| Regulation | Core obligation | Technical requirement |

|---|---|---|

| TCPA | Express written consent before texting | Automated consent capture with audit trail |

| GDPR / CCPA | Data minimization and subject access rights | Metadata-tagged archives with deletion workflows |

| FINRA / SEC | Business communication archiving | Tamper-evident logs with eDiscovery export |

| HIPAA | PHI protection in messaging | Encrypted channels plus access controls |

One underappreciated compliance boundary is device ownership. Message content determines whether a communication qualifies as a business record, not the device it was sent from. A broker texting a client from a personal iPhone is generating a regulated business record. BYOD policies do not create exemptions; they create gaps.

On the encryption side, Messaging Layer Security (MLS) rolled out broadly in 2026 with support from Google and Apple. MLS represents a meaningful advance in end-to-end encryption for group messaging. However, encryption protects the transport channel. It does not produce the centralized, auditable logs that FINRA or SEC examiners will request. Compliance teams need to understand that MLS and regulatory archiving are separate problems requiring separate solutions.

Preparing your organization for compliance

Preparation is where most organizations fall behind. They address consent workflows or archiving in isolation, without building the cross-functional architecture that regulators actually examine.

The foundational elements of a compliant mobile messaging program include:

-

10DLC registration: All application-to-person (A2P) SMS traffic in the U.S. must be sent through registered 10-digit long codes. Unregistered traffic is filtered by carriers and creates audit exposure. Core requirements include 10DLC registration, express consent documentation, opt-out mechanisms, and real-time archiving with preserved metadata.

-

Consent management: Double opt-in workflows that capture timestamp, IP address, and the exact consent language presented to the user. Single opt-in records rarely survive regulatory scrutiny.

-

Tamper-evident archiving: Archives must capture message content, metadata, timestamps, and attachments. Platforms must be engineered explicitly to capture ephemeral actions including edits and deletions. Screenshots are not compliant and are easily manipulated.

-

Customer-controlled encryption: Standard provider-managed TLS and disk encryption are not sufficient for data sovereignty. Audits flag reliance on provider-managed encryption as a failure point. Envelope encryption using BYOK, EKM, or HSM approaches gives organizations the key control that regulators expect.

-

Cross-department governance: Compliance, IT, legal, and security teams must share ownership of the messaging security program. Siloed ownership produces gaps that appear immediately under audit.

Pro Tip: Before selecting any archiving vendor, ask specifically whether the platform captures iMessage and WhatsApp natively, not through screen recording or agent-based workarounds. Native capture is the only method that produces defensible records for eDiscovery.

The identity layer is equally critical and frequently overlooked during preparation. Smishing attacks targeting employees do not require breaking encryption. They exploit trust. Building an identity verification framework that includes biometrics or hardware tokens at the authentication layer addresses the attack vector that encryption cannot.

Implementing controls and best practices

Execution requires translating policy into technical controls that operate continuously, not just during audit preparation cycles.

-

Deploy automated consent collection. Use double opt-in workflows that log the consent event with timestamp, channel, and the precise language the user agreed to. Store these records in an immutable archive separate from your messaging platform.

-

Implement a compliant archiving platform. The platform must capture message content, metadata, sender and recipient identifiers, timestamps, and attachments in real time. Edited and deleted messages must be preserved with version history. Capturing ephemeral messaging actions in compliance archiving is required to meet eDiscovery standards.

-

Replace manual spot checks with continuous monitoring. Legacy manual processes fail audits; near-real-time visibility is now expected by regulators. Automated compliance monitoring tools that flag consent violations, opt-out failures, or suspicious message patterns are no longer optional in financial services.

-

Enforce opt-out mechanisms rigorously. Every outbound message must include a clear opt-out path. Opt-out requests must be honored promptly and documented in the consent archive. Failure here is one of the most common TCPA enforcement triggers.

-

Deploy AI-driven smishing detection. Inbound smishing attacks targeting employees are a direct compliance risk. Credential theft through a phishing SMS can trigger breach notification obligations, regulatory inquiries, and reputational damage. Contextual phishing warnings and AI-powered impersonation detection at the device level intercept these attacks before they reach the credential-harvesting stage.

-

Integrate identity verification beyond transport encryption. Experts advise shifting from reliance on transport encryption alone to biometrics and hardware verification for messaging security. This is the control layer that stops AI-driven impersonation even when the message channel itself is encrypted.

Pro Tip: The MLS protocol can be configured with escrowed access for supervision without compromising end-to-end encryption. This architecture satisfies FINRA and SEC supervision mandates while maintaining message security for participants.

The comparison below illustrates the gap between legacy and current-generation compliance controls:

| Control area | Legacy approach | Current standard |

|---|---|---|

| Consent capture | Paper forms or checkbox | Automated double opt-in with immutable log |

| Archiving | Manual export or screenshots | Native real-time capture with version history |

| Monitoring | Periodic manual review | Continuous automated oversight with alerts |

| Encryption | Provider-managed TLS | Customer-controlled BYOK/EKM envelope encryption |

| Smishing defense | Email security tools | On-device AI filtering and impersonation detection |

Auditing and verifying your compliance posture

Verification is not a one-time event. Regulators in 2026 expect organizations to demonstrate ongoing compliance, not just point-in-time snapshots.

Continuous audit trail reviews should cover consent records, opt-out logs, archiving completeness, and any gaps in message capture. Testing archiving system integrity means verifying that metadata has not been altered and that the chain of custody for each record is intact. This matters enormously when responding to regulatory inquiries, FOIA requests, or eDiscovery demands.

Common pitfalls that surface during compliance verification include:

-

Incomplete BYOD coverage: Personal devices used for business messaging are frequently excluded from archiving scope, creating defensibility gaps.

-

Archiving latency: Systems that batch-archive on a 24-hour cycle cannot produce the near-real-time records regulators now expect.

-

Missing deletion logs: If the archive does not capture deleted messages with timestamps and actor identifiers, it will not satisfy eDiscovery requirements.

-

Static consent records: Consent records that do not reflect subsequent opt-outs or preference changes are a TCPA liability.

-

No smishing telemetry: Organizations that cannot demonstrate awareness of inbound messaging threats targeting their workforce face harder questions during security audits.

Regulators are no longer satisfied with evidence that a policy existed. They want evidence that the policy was enforced, monitored, and updated in response to real events. Compliance analytics that surface deviations in near-real-time are the difference between a defensible program and an enforcement action.

Updating procedures in response to regulatory changes and incident lessons learned should be a documented process, not an ad hoc reaction. Assign ownership, set review cycles, and maintain version-controlled policy documents that show examiners a living compliance program.

My take on where compliance teams are getting this wrong

I’ve spent considerable time working through how organizations in regulated industries approach mobile messaging compliance, and the pattern I keep seeing is the same. Teams invest heavily in outbound compliance, consent workflows, 10DLC registration, archiving platforms, and then treat inbound messaging threats as someone else’s problem.

That framing is wrong, and it is getting organizations into trouble. A smishing attack that successfully harvests credentials from a financial advisor’s iPhone does not stay contained. It triggers breach notification obligations, potentially exposes client data, and puts the organization in front of regulators asking why the threat was not detected. The attack chain from smishing to credential theft to lateral movement is well documented. Treating it as outside the compliance perimeter is a gap that examiners are increasingly aware of.

The second issue I see is over-reliance on encryption as a compliance signal. Encryption is necessary. It is not sufficient. I’ve watched organizations point to their MLS or RCS deployment as evidence of a mature security posture, while having no identity verification layer and no visibility into AI-driven impersonation attempts targeting their people. Encryption protects the pipe. It does not verify who is on the other end.

The organizations that are genuinely ahead of this problem have automated monitoring, native archiving that captures ephemeral message actions, and on-device smishing detection running in parallel. They treat mobile messaging as a full-spectrum compliance surface, not just an outbound channel to manage.

— Sophie

How SmishAlert addresses the full compliance surface

Organizations that have addressed outbound compliance but lack visibility into inbound smishing threats are carrying regulatory and security exposure they may not fully recognize. SmishAlert is built specifically to close that gap.

SmishAlert’s platform delivers on-device AI filtering and one-tap reporting that gives security teams real-time visibility into smishing campaigns targeting employees, executives, and mobile devices across SMS, iMessage, and other messaging channels. Unlike email-focused security tools, SmishAlert operates at the messaging layer where these threats actually arrive.

For compliance teams, SmishAlert provides the telemetry needed to demonstrate awareness of inbound messaging threats during regulatory inquiries. The platform requires no MDM deployment, which removes a significant barrier for organizations managing BYOD environments. You can explore phishing protection without MDM to understand how that deployment model works in practice. User-reported attacks are analyzed and correlated in real time, helping security teams identify broader campaigns before they escalate into breach notification events.

FAQ

What regulations govern mobile messaging security in the U.S.?

The primary frameworks are the TCPA for consent and opt-out obligations, GDPR and CCPA for data protection, and industry rules like FINRA and SEC regulations requiring communication archiving. HIPAA applies when protected health information is transmitted over messaging channels.

How much can TCPA violations cost per text message?

TCPA violations carry fines between $500 and $1,500 per unauthorized message, and those penalties apply to each individual text sent without proper consent.

Is encryption alone sufficient to meet messaging compliance requirements?

No. Encryption protects the communication channel but does not produce the auditable logs, tamper-evident archives, or identity verification controls that regulators require. Compliance demands both secure transport and defensible recordkeeping.

What is the difference between archiving and screenshots for compliance purposes?

Screenshots are not compliant for eDiscovery or regulatory recordkeeping because they can be manipulated and do not capture edits or deletions. Compliant archiving platforms capture message content, metadata, timestamps, and ephemeral actions natively and in real time.

How does smishing create regulatory exposure for compliance teams?

A successful smishing attack that results in credential theft can trigger breach notification obligations and regulatory inquiries. Organizations that cannot demonstrate awareness of inbound messaging threats targeting their workforce face harder scrutiny during security audits.